The K-Beauty Trinity: Manufacturing, Logistics, and the Rise of the Indie Brand

Beyond its cultural popularity, K-beauty represents a triumph of the “Trinity” industrial model, where shared manufacturing and logistics enable indie brands—small, independent companies without their own factories—to disrupt conglomerate dominance. This modular ecosystem allowed the sector to survive a Chinese consumer boycott triggered by geopolitical tensions in 2017 and rapidly pivot exports to the United States. Consequently, it offers policymakers a blueprint for building economic resilience: one grounded in shared infrastructure and regulatory frameworks that match the speed of innovation.

Introduction

When people think of the “Korean Wave,” K-pop stars like BTS and Netflix shows like Squid Game often come to mind. But for an economist, one of Korea’s most important success stories is not on a stage or TV: it is in the industrial ecosystem.

K-beauty, broadly encompassing the country’s cosmetics sector, has quietly transformed into a key pillar of the South Korean economy. Exports have surged to over $10 billion as of 2025, positioning South Korea as a top global exporter alongside France and the United States. These record-breaking numbers hide a dramatic story of near collapse under geopolitical pressure and structural rebirth. K-beauty has attained such global success despite facing a demand crisis in its Chinese market and adapting by adopting a trifurcated industrial model, which separately compartmentalizes manufacturing, logistics, and marketing. The impact of this model provides key lessons for governments seeking to support nascent or fragile domestic industries with interventions that support market entrants and expedite regulatory processes.

The Catalyst: The China Shock

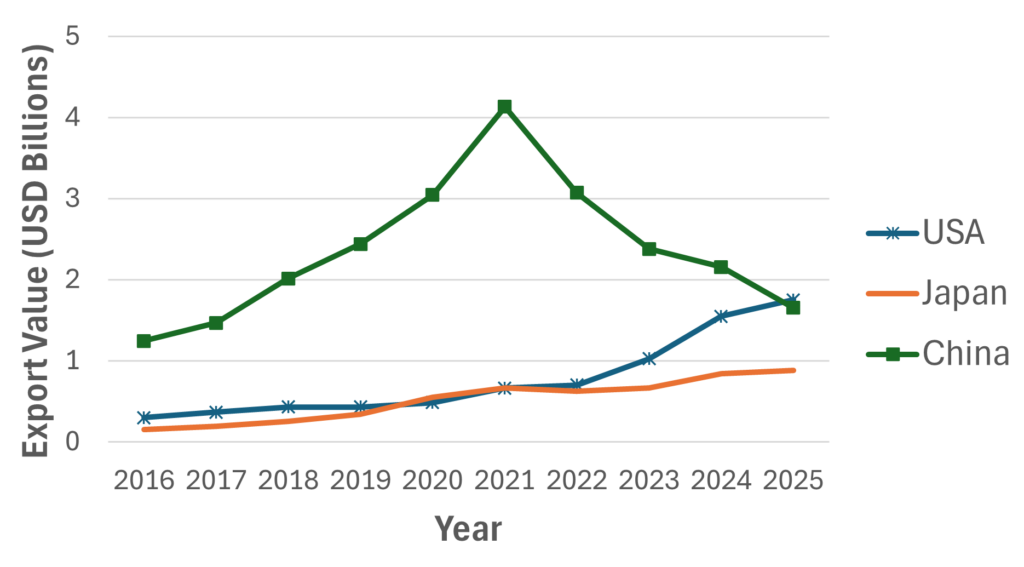

To understand the current success of K-beauty, one must first understand its greatest crisis. From its emergence, the Korean cosmetics industry was dangerously reliant on demand from the neighboring Chinese market. At its peak, nearly 50% of all Korean cosmetic exports flowed to China (see Figure 1). However, geopolitical tensions rose in 2017 following the deployment of THAAD, a U.S. anti-missile system, in South Korea. Beijing viewed such military action as a threat to its security interests and retaliated against Korea with severe economic implications.

Korean exports plummeted. The “Big 2” conglomerates, AmorePacific and LG H&H—which had invested heavily in physical stores and marketing in China—took a massive hit. This crisis acted as a catalyst for “creative destruction,” forcing the industry to decouple from China and target the North American market.

However, to pivot to and survive in the highly competitive U.S. beauty market, long dominated by established Western conglomerates like L’Oréal, Estée Lauder, and Procter & Gamble, the industry had to change how it operated. It moved from a rigid, giant-led model to an agile, trend-driven model led by small, digitally-native brands. Trade data confirms this massive shift. While exports to China have declined, exports to the U.S. have skyrocketed to nearly $1.8 billion, doubling from 2022 (see Figure 1).

Figure 1: South Korea Cosmetics Export Trends (2016-2025)

Note: Author’s calculation with Korea Customs Service data. Data reflects customs value for Korean exports under HTS Code 3304 (Beauty, makeup, and skin care preparations). Values are expressed in billions of U.S. dollars.

The Trinity: A New Industrial Ecosystem

The industry’s recovery and growth were not driven by a single company, but by the fostering of a modular ecosystem best represented by the name “K-Beauty Trinity.” This trifurcated system splits the traditional supply chain into three specialized players: the manufacturer, the distributor, and the marketer. While in the traditional beauty industry, large conglomerates like L’Oréal or Estée Lauder vertically integrate the entire value chain from research and development (R&D) labs to marketing operations, the Trinity model unbundled the value chain into three open platforms. In doing so, it allowed entrants to compete in a market that traditionally required billions in capital and decades of brand-building.

1. The Manufacturer: The “AWS” of Beauty

The first pillar of the Trinity is the Original Design Manufacturer (ODM). In the past, the beauty industry operated as an oligopoly where only giant and generally already-established corporations could afford the millions of dollars needed to build factories and labs. South Korea disrupted this by industrializing the backend and offering platforms to aspiring market entrants.

In the Korean value chain, companies like Cosmax and Kolmar Korea function like Amazon Web Services (AWS) for skincare. Just as a tech startup rents servers from hyperscalers like AWS, a beauty startup can rent research and production from these ODMs, which maintain extensive libraries of ready-made formulas. Such benefits allow entrepreneurs to launch a brand without deep expertise in chemistry. While ODMs handle formulation science, brands can thus devote their resources to differentiation via trend identification, ingredient storytelling, and packaging design. A brand like Beauty of Joseon, for example, doesn’t invent new molecules. It identifies that Western consumers want traditional Korean herbal ingredients in modern formats, then commissions ODMs to formulate accordingly. Ultimately, the R&D remains shared between customer brands while brands’ particular insights become proprietary.

This platform manufacturing model has lowered the barrier to market entry to nearly zero. Startups can now order small batches of as few as one thousand units, eliminating the minimum-scale problem that traditionally kept small brands out of manufacturing. A founder can test a product concept with a small batch, gauge market response through social media, and only scale production if demand materializes. It has also created an ecosystem of “Fast Beauty.” While Western legacy brands typically take years to bring a product from concept to shelf, Korean ODMs can execute this cycle in less than six months, allowing Korean indie brands to capitalize on social media trends instantly.

2. The Distributor: The “FedEx” of Beauty

Manufacturing was only half the battle. To sell in the U.S., small Korean brands faced a massive logistical hurdle. Shipping individual orders across the Pacific was too slow, and renting warehouses in California was too expensive.

The emergence of the company Silicon Two, the second pillar of the “Trinity” model, alleviated this bottleneck. Acting as a global fulfillment platform, Silicon Two buys inventory directly from Korean brands and stores it in its own local warehouses in the U.S., Europe, and Southeast Asia. In doing so, it effectively democratizes logistics by removing each company’s overhead cost of building logistics centers. It simultaneously solves the cash flow problem for small startups by buying stock upfront and accelerates delivery by maintaining stocks significantly closer to the centers of demand. By integrating manufacturing as represented by ODMs with logistics through Silicon Two, the ecosystem removed the operational friction of exporting, allowing thousands of micro-firms to flood the global market.

3. The Marketer: The Rise of Indie Brands

The final pillar emerges through the indie brand. Freed from the burden of manufacturing and logistics, these small companies focus all of their resources on branding and digital marketing. The ability of entrants to do so has birthed a new generation of agile, digitally-native brands that operate with a fraction of the headcount of traditional conglomerates. They do not own factories. They do not own trucks. They simply own data and customer relationships. By leveraging social media platforms like TikTok and Instagram, they identify micro-trends and internet buzzwords such as “glass skin” or “barrier repair” and rapidly commission products from ODMs to meet that demand.

The efficiency of the “Trinity” model is best illustrated by the success of independent brands that have outperformed legacy giants through laser-focused niche targeting. For instance, Beauty of Joseon achieved viral success in the U.S. by reintroducing traditional Korean herbal ingredients to Western consumers and addressing the common complaint of white cast in sunscreens. Leveraging advanced chemical filters from Korean ODMs, their “Relief Sun” sunscreen became a massive hit. Similarly, COSRX built a loyal following by prioritizing clinical effectiveness and clear ingredient lists, taking advantage of the unique popularity of snail mucin. Driven by user-generated content rather than costly ad campaigns, their “Advanced Snail 96 Mucin Power Essence” became so successful that the brand was eventually acquired by industry giant AmorePacific. Finally, Tirtir demonstrated the agility of the ODM model by rapidly expanding its “Mask Fit Red Cushion” foundation shade range from a limited selection to forty shades in response to feedback from Black beauty influencers. This quick pivot allowed Tirtir to capture the number one spot in Amazon’s foundation category, a distinction previously considered unattainable for a Korean brand in this market.

The Result: The Economics of “Masstige”

This new industrial structure has created a compelling economic value proposition known as “Masstige,” or prestige quality at mass prices. Because ODMs achieve massive economies of scale by producing billions of units annually, they drive down unit costs significantly. This allows indie brands to sell high-quality serums and creams in the $10-$20 price range. Particularly in an inflationary U.S. economy where consumers often trade down to cheaper, lower-quality products, Korean cosmetics offer a unique alternative: trading down in price without trading down in efficacy.

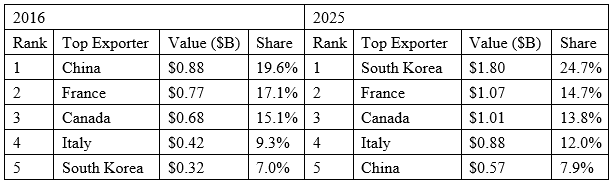

As a result of this trend, U.S. cosmetic imports have undergone a radical transformation over the last eight years. In 2016, the market was dominated by traditional manufacturing giants, with China leading the pack and South Korea trailing in fifth place. By 2025, South Korea had ascended to the number one spot, capturing 24.7% of the total import market with a value of $1.8 billion.

Table 1: Top 5 U.S. Beauty Imports by Origin (2016 vs. 2025)

Note: Author’s calculation with U.S. International Trade Commission data. Data reflects the general customs value for U.S. general imports under HTS Code 3304 (Beauty, makeup, and skin care preparations). Values are expressed in billions of U.S. dollars.

Policy Implications: From K-Beauty to a Scalable Blueprint

The Trinity model and its success offer a template that policymakers in other countries can study and adapt. Two lessons stand out.

First, the model challenges the conventional industrial policy of supporting large firms through subsidies or protection. Shared infrastructure, rather than direct support, drove K-beauty’s recovery after the China shock. In mimicking this approach, governments seeking to grow an export sector can look for opportunities to fund or de-risk the shared backend—including factories, labs, and logistics hubs—rather than picking individual winners at the brand level. For example, Southeast Asian governments can apply such a policy to their domestic food and beverage industries, where thousands of small producers have distinctive products but lack the shared cold-chain logistics and regulatory compliance infrastructure to reach Western retail shelves. Shared platforms could spread risk, lower barriers, and generate positive spillovers that benefit the entire ecosystem.

Second, governments can mirror the less visible but equally important factor in K-beauty’s rise: the regulatory environment. South Korea’s Ministry of Food and Drug Safety uses a “negative list” system for general cosmetics under which anything not explicitly prohibited is allowed, and no pre-market approval is required. This model has the potential to be especially impactful for the U.S. market, in which the Food and Drug Administration currently lacks a dedicated fast-track approval process for cosmetics with functional claims, leading to products getting stalled before market entry. The adoption of a negative list model similar to Korea’s can expedite regulatory approval without compromising safety standards. The resultant increase in regulatory speed could, in turn, reinvigorate the competitiveness of U.S. brands. Policymakers in other countries should also examine whether their regulatory timelines match the speed of innovation their industries need and adjust policies accordingly.

Conclusion

The K-beauty turnaround stands as a textbook example of industrial resilience. By pivoting from a centralized, conglomerate-heavy structure to a modular, platform-based ecosystem, South Korea built an industry capable of withstanding geopolitical shocks. The lesson for policymakers is clear. Economic resilience does not come from protecting large national champions, but from building shared backend platforms and designing regulatory frameworks fast enough to let thousands of small innovators compete on a global stage. Any export-oriented sector with high fixed costs and fragmented producers could benefit from asking the same question the Korean cosmetics industry answered after 2017: what shared infrastructure would allow small firms to do what only large ones can do today?

. . .

Munseob Lee is an Associate Professor of Economics and the Lawrence and Sallye Krause Chair in Korean Studies at the UC San Diego School of Global Policy and Strategy, where he also serves as director of the Korea-Pacific Program. In his career, he has served as a short-term consultant at the World Bank and a visiting fellow at the Asian Development Bank.

Image Credit: K-beauty expo by Kintexsw, CC BY-SA 4.0, via Wikimedia Commons

{kind=link}